Alcohol trade regulation in Canada falls under provincial jurisdiction. Each province controls importation, distribution and, in most cases, retail sales through a provincial Crown corporation (either a full monopoly or a hybrid model).

Market access therefore cannot be planned at the national level. It must be structured province by province, through an authorized agent and a formal submission process. In a context of stagnant volumes, mastering product offering, pricing and distribution channels becomes critical.

For a foreign company, direct market access is rare. In many provinces, entry requires:

Note: In Canada, retail sales outside the HORECA channel may occur either through provincially operated liquor stores, authorized grocery retailers, or directly at production sites (wineries, cideries, distilleries, breweries). In this article, the term “grocery” refers to supermarkets and food retailers holding a specific provincial license to sell alcohol. A “convenience store” refers to a smaller retail outlet authorized to sell certain alcohol categories under provincial regulations.

During the fiscal year from April 1, 2023 to March 31, 2024, total alcoholic beverage sales in Canada reached CAD 26.2 billion, representing a slight decrease of -0.1% in value compared to the previous year.

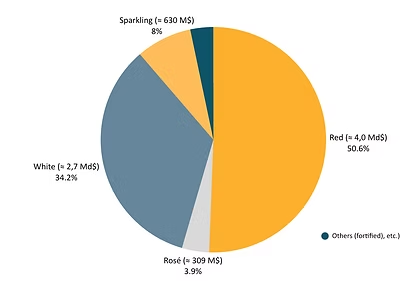

For the 2022–2023 fiscal year, the structure of the wine market (in value terms) was as follows:

For 2023–2024, Statistics Canada reports the total value of wine sales (CAD 7.8 billion) and total volumes (476 million litres), but does not yet provide a detailed breakdown by red, white and rosé wine in its latest release.

Average wine consumption in Canada in 2024 stands at approximately 14 litres per capita (age 15+), with significant provincial variations: Québec leads at 22.3 litres per capita, followed by British Columbia at 14 litres and Ontario at 12 litres.

Québec residents also remain the highest spenders per capita on wine, at CAD 374 per person, compared to CAD 215 in Ontario, CAD 191 in British Columbia, CAD 162 in Alberta and CAD 161 in New Brunswick.

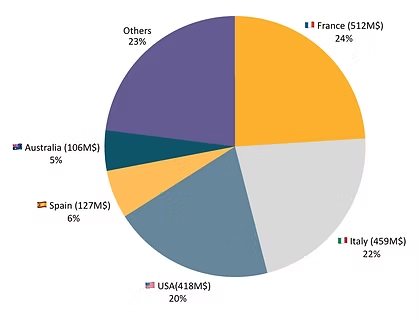

In 2024, the main countries of origin of wine imports into Canada (by value) are:

The Canadian wine market remains dominated by red wines, with sustained demand for well-known international grape varieties such as Cabernet Sauvignon, Merlot, Pinot Noir, Chardonnay and Sauvignon Blanc. The core of the market sits largely within an accessible premium price range, typically between CAD 13 and 18 per bottle, where a significant share of volumes is concentrated.

Price construction is a critical factor: federal excise duties, provincial mark-ups, logistics and taxation can significantly increase the final shelf price compared to the ex-cellar price. Upfront pricing calibration is therefore essential to remain competitive within the targeted price segment.

Canadian consumers are curious and open to discovery, but highly attentive to value for money. Country of origin remains a differentiating factor, particularly for European wines. In practice, products that perform well combine clarity (clearly identifiable grape variety or well-known appellation), a price positioning aligned with market expectations, and marketing support adapted to the chosen distribution channel.

Do you have a project in mind or would you like to learn more about our services? Get in touch today for a complimentary consultation with one of our experts.

Ontario combines a historic public monopoly (the LCBO) with a gradual retail liberalization since 2024. The LCBO remains the primary importer and wholesaler.

Since September 5, 2024, beer, cider, wine and ready-to-drink (RTD) beverages may be sold in convenience stores, and subsequently in grocery stores and large retail outlets. This expansion applies regardless of country of origin; however, products must still transact through the LCBO and an authorized agent.

For a foreign producer, two elements are critical:

In Ontario, product assortment is managed by the LCBO through regularly published Calls for Products (CFPs) on its supplier portal. These calls specify target categories, price segments, technical criteria and logistical requirements. Submissions must be filed by a registered agent and are evaluated based on commercial potential and fit within the existing portfolio. Current calls and supplier information are available on the LCBO supplier portal under the Merchandising / Calls for Products section.

In Ontario, two access models coexist within the LCBO system:

Québec operates under a strong public monopoly: the SAQ (Société des alcools du Québec) holds exclusive authority over the importation and distribution of alcoholic beverages. It is the central market actor.

The SAQ is one of the largest purchasers of imported wines in Canada, particularly French wines, and holds significant negotiating power with international producers. Listing procedures and supplier management are handled through the SAQ-B2B supplier portal.

As part of its 2026–2027 assortment plan, the SAQ publishes product calls and category priorities, along with detailed selection criteria. These documents are essential when preparing a submission and typically include links to open calls and targeted product classes.

Wines and spirits are sold to Québec consumers through a network of approximately 410 SAQ stores (classic, express and selection formats) and 430 agencies (SAQ-authorized retail outlets operating within private businesses).

In Québec, a foreign producer cannot sell directly and must work through an authorized local agent. The agent submits products, manages price positioning, handles administrative procedures and oversees commercialization. Their role is strategic, as access to the Québec market largely depends on their ability to successfully list and actively promote products with the SAQ.

In Québec, two main access routes coexist within the SAQ system:

SAQ Store Listing

Private Importation (IP)

Despite its name, private importation is not independent from the monopoly system. The product still transits through the SAQ but is not listed in retail stores. It is exclusively destined for restaurants and bars (HORECA) and private orders handled through agents.

This channel is often used to test the market or position premium and niche cuvées with a more targeted strategy.

Regarding the grocery channel, a specific requirement applies: to be sold outside the SAQ network, wine must be bottled in Québec. This condition governs access to that retail circuit and may require a localized industrial strategy.

The Québec model remains strongly influenced by political and regulatory decisions. For example, in March 2025 the SAQ announced the removal of U.S. products from its network and later clarified in February 2026 that certain inventories could be sold under specific conditions, while maintaining a suspension of new orders.

In all cases, the agent’s role remains central: they guide the producer toward the most appropriate entry channels based on portfolio profile, price positioning, available volumes, marketing budgets and development objectives. The choice between regular listing, specialty programs or the HORECA channel must be part of a structured strategy developed in advance rather than a simple administrative step.

Outside Québec and Ontario, importation remains largely centralized through a provincial authority. Alberta has a more liberalized retail environment, but product access remains regulated.

For an exporter, the key is not only to identify retail outlets, but to understand:

Beyond import mechanisms and price construction, understanding distribution channels is essential to structuring a successful market entry strategy.

The Canadian alcoholic beverage market is primarily organized around three main channels:

This is the structuring channel in most provinces (SAQ, LCBO, NSLC, ANBL, etc.). These organizations control importation and operate physical retail networks, often complemented by online platforms.

Market access is obtained through a formal submission and listing process.

In certain provinces (notably Ontario, Alberta, British Columbia and, to a lesser extent, Québec), licensed wine shops, supermarkets, large retail chains and convenience stores are authorized to sell specific alcohol categories.

This channel introduces an additional competitive dimension, particularly in terms of pricing flexibility and shelf visibility.

On-premise consumption represents a significant lever, particularly for premium wines and spirits. Supply to the HORECA channel typically occurs through the provincial authority or an authorized distributor. In some provinces, a local agent is required to officially represent the producer before the public authority and structure commercialization efforts.

In summary:

With more than 70% of wine consumed in Canada being imported, the country remains a strategic market for European producers. However, dynamics are shifting: volumes are slightly declining while value remains stable, reflecting stronger price pressure and increased competition.

Several trends currently shape the market:

The market remains dominated by major international groups and established portfolios, intensifying competition for shelf space.

Despite gradual retail liberalization in certain provinces (notably Ontario), importation and distribution remain highly regulated by provincial authorities.

In practice, Canada is not a single unified market but a provincial mosaic. Success requires a structured, province-by-province approach integrating pricing strategy, channel selection and close collaboration with a local agent.

Entering the Canadian market depends on more than product quality alone. It requires identifying priority provinces, calibrating price positioning, selecting the appropriate channel (monopoly network or private import/HORECA), and most importantly, partnering with a competent agent aligned with the producer’s strategy.

Adexia supports producers and industrial players through a structured approach:

Our objective is not simply to introduce a product, but to build a sustainable and profitable presence in the Canadian market.

The Canadian food and beverage market is mature, highly competitive, and strongly intermediated. Growth is ...

SMEs and Mid-Sized Companies: Have You Considered External Growth to Accelerate Your Expansion in Canada ...

Canada is Opening the Door to Strategic Investment in Energy, Infrastructure and Critical Resources Thanks ...

In today’s global landscape, where medical innovation and access to strategic markets are critical challenges, ...

Canadian engineering is entering a pivotal decade: rarely has the country mobilized so much public ...

In 2025, Ontario confirms its position as Canada’s leading economic powerhouse. With a dynamic population, ...