The Canadian food and beverage market is mature, highly competitive, and strongly intermediated. Growth is driven less by increasing volumes than by brands’ ability to differentiate themselves, justify their pricing, and secure access to the right distribution channels.

For foreign companies, market access depends as much on regulatory compliance as on commercial positioning. Imports are governed by a federal framework covering food safety, licensing, duties and taxes, quotas, traceability, and mandatory labelling requirements. Commercial execution, however, remains largely provincial, particularly in Quebec, where language regulations reinforce the importance of French on packaging and commercial materials.

Direct market entry is rarely the most realistic approach in the early stages. Access is typically achieved through an importer-distributor, broker, specialized wholesaler, or local partner capable of opening the right channels. In this context, success depends on thorough preparation: selecting the appropriate route to market, building a competitive landed cost structure, ensuring regulatory compliance, identifying the right local partner, and prioritizing target provinces.

Canada’s food and beverage industry remains one of the country’s key industrial sectors. In 2024, food and beverage manufacturing sales reached CAD 173.4 billion, representing approximately 7.5% of national GDP and confirming the strategic importance of the industry within the Canadian economy.

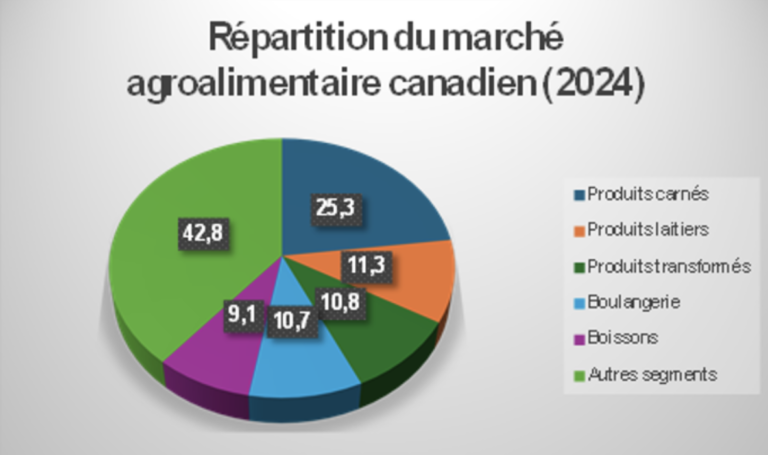

Within domestic food processing, the main industrial segments include meat products, dairy products, grain and oilseed milling, bakery products, and beverages. While this structure reflects the weight of major categories within Canada’s manufacturing base, it should not be confused with the structure of market opportunities accessible to foreign companies.

Breakdown of Food and Beverage Manufacturing Sales in Canada, 2024

For international entrants, the challenge is less about targeting the largest industrial segments than identifying the categories where an imported product can offer clear differentiation, a coherent price positioning, and sufficient turnover potential for distributors.

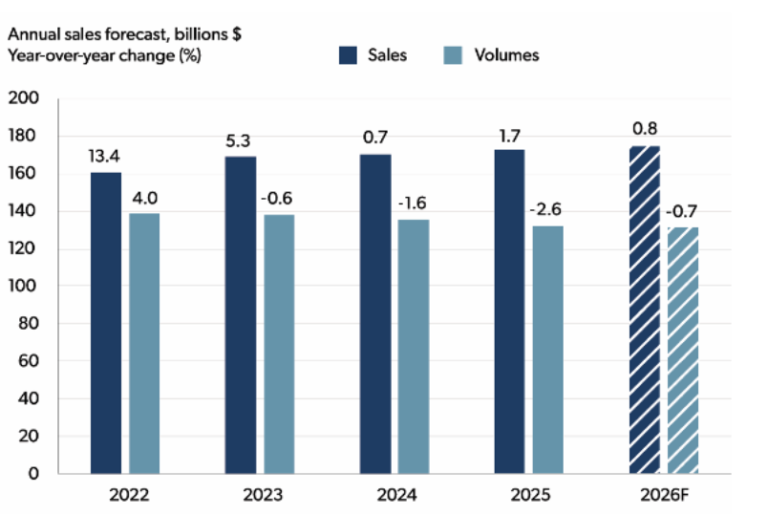

Current market dynamics reinforce this selective approach. According to Farm Credit Canada (FCC) forecasts for 2026, industry sales are expected to grow by only 0.8%, while volumes are projected to decline by 0.7%. This divergence reflects a broader structural trend: growth is no longer primarily driven by increased consumption, but rather by pricing effects, the expansion of higher-margin categories, and companies’ ability to protect profitability.

Evolution of Sales and Volumes in the Canadian Food and Beverage Industry (2022–2026F)

International suppliers must therefore offer products that demonstrate clear commercial relevance for the targeted channel: expected turnover, distributor margins, competitive landed pricing, differentiation or innovation, clarity of positioning, and the ability to integrate into already established categories.

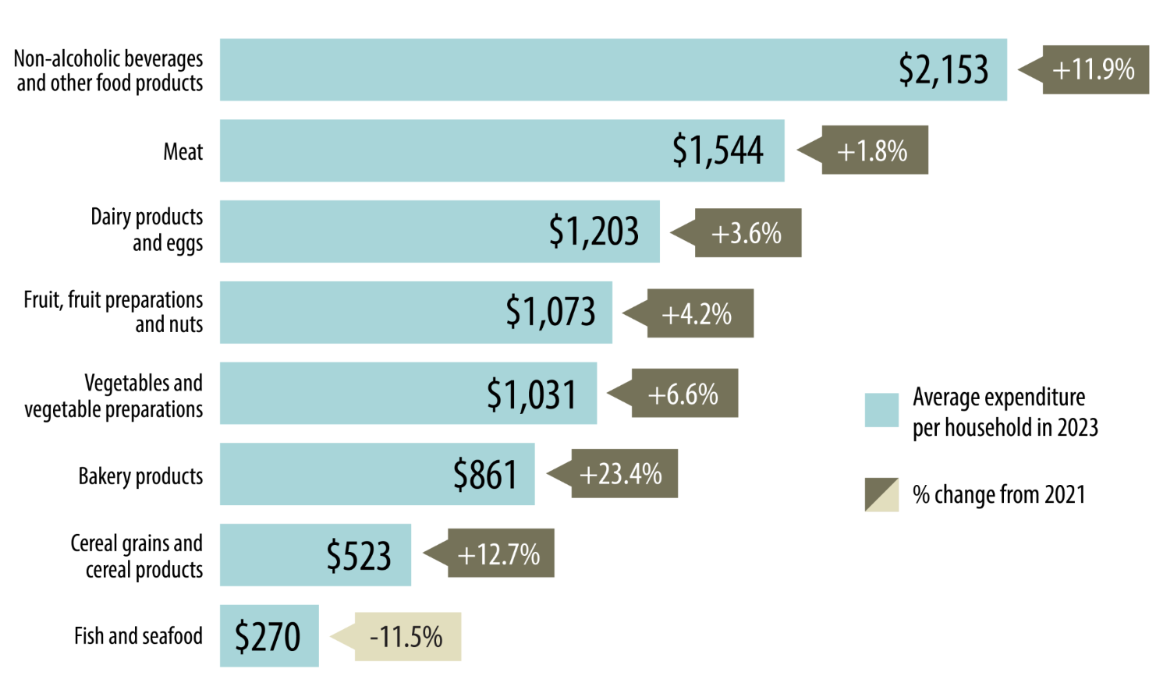

The latest detailed data available on the composition of Canadian household food spending dates back to 2023.

It shows demand structured around non-alcoholic beverages and other food products, meat, dairy products and eggs, fruits, vegetables, bakery products (+23.4%), and cereal products (+12.7%).

In 2024, however, consumption trends confirmed increased price sensitivity. Sales from food and beverage retailers reached CAD 137.0 billion, up 1.8%, while food purchases in general merchandise stores — such as Walmart, Costco, and Dollarama — rose by 8.9% to CAD 45.3 billion. This shift reflects growing consumer trade-offs toward value-oriented formats, without undermining the overall depth of Canadian food demand.

Evolution of Canadian Household Food Expenditures by Category (2021–2023)

The slowdown in food inflation has not eliminated price sensitivity. Grocery prices increased by 2.2% in 2024, compared to 7.8% in 2023. While inflationary pressure is easing, consumers remain highly attentive to value for money, promotions, and budget-oriented formats.

This shift does not close the market to differentiated products, but it does require a clearer value proposition. The most relevant opportunities are those combining convenience, clear usage, health or nutritional benefits, flavour differentiation, and coherent pricing.

For foreign companies, the segments worth monitoring include non-alcoholic beverages, ready-to-eat products, snacks, differentiated bakery products, prepared meals, protein alternatives, and selected health or plant-based offerings. The challenge is therefore not to target the largest categories by volume, but rather the sub-categories where an imported product can quickly demonstrate its value through sufficient turnover, clear differentiation, acceptable landed pricing, and relevance for the targeted distribution channel.

The Canadian food and beverage market relies on a concentrated distribution landscape, highly structuring intermediaries, demanding listing processes, and a commercial execution model that remains strongly regionalized. For foreign companies, success depends less on the attractiveness of the product alone than on the ability to identify the right channel, the right local partner, and the right market entry sequence.

Access to Canadian consumers is largely controlled by a limited number of retailers. The food retail market is dominated by a handful of major groups — Loblaw, Empire / Sobeys, Metro, Walmart, and Costco — which account for a significant share of sales and largely shape listing conditions.

This concentration represents a major commercial barrier for new entrants. Entering the market is not simply about finding a buyer; companies must convince highly selective purchasing teams in an environment where shelf space, product turnover, margins, logistical reliability, and promotional support are critical factors.

The Competition Bureau Canada reinforces this assessment, noting that the Canadian grocery industry remains highly concentrated and that most consumers purchase food products from stores owned by a limited number of large groups. This concentration remains particularly high: in their respective 2025 fiscal years, Loblaw, Empire / Sobeys, and Metro reported combined sales of approximately CAD 117 billion. While this figure includes certain non-food activities such as pharmacy and fuel sales, it illustrates the commercial weight of Canada’s leading retailers when dealing with new market entrants.

In practice, direct access to major retail chains is rarely realistic for a foreign SME, particularly during the early stages of market entry. Product listings often rely on local intermediaries capable of presenting the product to buyers, managing import procedures and compliance requirements, and activating the right commercial accounts.

Three types of players are particularly important in this ecosystem: the importer-distributor, which manages importation, logistics, and distribution; the broker or sales agent, which facilitates access to retail buying teams without necessarily carrying inventory; and specialized wholesalers, particularly in foodservice, HORECA, or differentiated product categories.

Choosing the right partner is therefore not merely an administrative step. It directly impacts commercial credibility, geographic coverage, access to target accounts, quality of market execution, and the ability to convert initial interest into recurring orders. A distributor poorly aligned with the product category or channel can slow market entry just as much as the right partner can accelerate it.

Food retail offers the greatest volume potential, but it is also the most demanding channel. Major retailers impose strong pricing pressure, high turnover expectations, and often significant promotional investments. For foreign brands, targeting national retail chains too early can be premature if positioning, landed pricing, and local brand awareness have not yet been validated.

Foodservice often represents a more accessible entry point. In 2025, according to Statistics Canada, sales from foodservice establishments and drinking places reached CAD 101.4 billion, up 5.6% from 2024. Quick-service restaurants alone accounted for CAD 47.3 billion, representing 46.6% of the total market. For foreign companies, this channel provides an opportunity to test product adoption, build initial commercial traction, and develop manageable volumes before expanding into retail.

This channel is particularly relevant for premium products, differentiated ingredients, non-alcoholic beverages, high-quality frozen products, ready-to-use solutions, and food innovations requiring a demonstration phase. It allows companies to refine positioning and gather market feedback before negotiating broader retail listings.

Specialty channels — including gourmet retailers, health-focused stores, ethnic networks, regional distributors, and targeted e-commerce platforms — can also serve as effective entry points. Their value lies less in immediate scale than in their ability to validate a product offering with more targeted consumer segments.

Canada should not be approached as a homogeneous market. While imports and food safety are governed by a federal framework, commercial execution remains largely provincial, shaped by local distribution networks, available partners, language requirements, consumer habits, and logistics.

Quebec can represent a relevant entry point for European companies, particularly for premium, health-focused, plant-based, non-alcoholic beverage, or strongly branded European products. Montreal plays a central role as both a logistical and commercial hub for Eastern Canada. In 2025, the Port of Montreal handled 34.3 million tonnes of cargo, with containerized traffic increasing by 3.6%, confirming its importance in international trade flows.

Ontario follows a different logic: scaling and commercial expansion. The province concentrates a dense ecosystem of processors, distributors, national buyers, brokers, logistics platforms, and major accounts. According to provincial data, Ontario accounts for approximately 42% of Canada’s food and beverage GDP, making it a natural platform for targeting national retail, foodservice, structured distributors, or industrial partnerships.

In a progressive market entry strategy, Quebec can therefore serve as an initial commercial testing ground, while Ontario often becomes the province for consolidation and scale-up. The choice of entry province directly impacts partner selection, distribution strategy, language adaptation, logistics costs, and overall development sequencing.

The Canadian food and beverage market offers real opportunities, but they remain selective. The most promising segments are not always the largest by volume, but rather those where a foreign offering can demonstrate clear value for distributors, consumers, or industrial partners.

The main opportunity areas can be grouped into five key categories:

The Canadian opportunity is real, but it requires precise commercial execution: distributor margins, product turnover, competitive landed pricing, regulatory compliance, logistical reliability, and relevance for the targeted channel all remain critical success factors.

Entering the Canadian food and beverage market requires selecting the right entry model based on the targeted channel, landed pricing in Canada, the company’s export maturity, and its ability to support the market commercially.

Several approaches can be considered:

Local importer-distributor: often the most suitable model during the initial phase. It allows companies to test the market, limit initial risk, and gain access to established retail, foodservice, or specialty distribution networks.

Broker or specialized sales agent: relevant for companies seeking greater control over pricing strategy and relationships with targeted accounts. This model, however, requires stronger internal capabilities in logistics, compliance, and commercial follow-up.

Foodservice and specialty channels: a progressive entry route for premium, innovative, functional, or strongly differentiated European products. These channels make it possible to test market acceptance, refine positioning, and build commercial proof points before expanding into retail.

A phased provincial approach: Quebec can serve as an initial validation market for differentiated offerings, while Ontario often represents the next stage for structuring and scaling commercial operations.

Adexia supports food producers, manufacturers, and brands in structuring their entry into the Canadian market through a practical, market-driven approach.

Support may include:

Alcohol trade regulation in Canada falls under provincial jurisdiction. Each province controls importation, distribution and, ...

SMEs and Mid-Sized Companies: Have You Considered External Growth to Accelerate Your Expansion in Canada ...

Canada is Opening the Door to Strategic Investment in Energy, Infrastructure and Critical Resources Thanks ...

In today’s global landscape, where medical innovation and access to strategic markets are critical challenges, ...

Canadian engineering is entering a pivotal decade: rarely has the country mobilized so much public ...

In 2025, Ontario confirms its position as Canada’s leading economic powerhouse. With a dynamic population, ...